If someone told you the government would hand you up to S$230,000 toward your first home, you'd probably assume there's a catch. And there is — sort of. But for first-time HDB buyers in Singapore in 2026, stacking CPF housing grants to the headline figure of S$230,000 is genuinely real money, not a marketing gimmick. The trick is knowing exactly which grants you qualify for, how they layer on top of each other, and the handful of decisions that separate the couples who max out the stack from those who leave six figures on the table.

This guide breaks down the three CPF housing grants every first-timer should know — the Enhanced CPF Housing Grant (EHG), the Family Grant, and the Proximity Housing Grant (PHG) — with eligibility tiers, worked scenarios, and the Budget 2026 cost-of-living support that cushions your most expensive year as a new homeowner. By the end, you'll know precisely what your number is.

The Headline Number: S$230,000 — But Read the Fine Print

Let's start with the math that makes the headlines. For a first-timer family buying an HDB resale flat on the open market, three grants stack to a maximum of S$230,000:

| Grant | Family max | Singles max | Available on |

|---|---|---|---|

| Enhanced CPF Housing Grant (EHG) | S$120,000 | S$60,000 | BTO and resale |

| CPF Housing Grant ("Family Grant") | S$80,000 | S$40,000 | Resale only |

| Proximity Housing Grant (PHG) | S$30,000 | S$15,000 | Resale only |

| TOTAL (resale) | S$230,000 | S$115,000 | — |

Before you start mentally spending it, here are the four framing truths that almost every viral "S$230K free money" post glosses over:

- The full S$230K only exists for resale buyers. If you're buying a new BTO or Sale of Balance flat, you get the EHG only — a maximum of S$120,000 for families. The Family Grant and Proximity Housing Grant are open-market resale instruments. So the "free money" headline is, fundamentally, a resale story.

- Grants are credited to your CPF Ordinary Account — not paid as cash. They reduce the cash and CPF you draw down to buy the flat. Think of them as down-payment firepower, not a windfall you can spend on a renovation or a holiday.

- Grants must be refunded with accrued interest when you sell. When you eventually sell, the grant amount plus the interest it "would have earned" in your CPF goes back into your CPF account. You don't lose it — it stays in your retirement pocket — but it's not a permanent gift.

- An HFE letter is mandatory first. The HDB Flat Eligibility (HFE) letter pre-confirms your grant eligibility and loan amount. You need it before you can exercise an Option to Purchase on a resale flat or apply for a BTO. Get it first, always.

Here's how the eligibility logic actually flows:

Now let's pull each grant apart.

Grant 1 — The Enhanced CPF Housing Grant: Up to S$120,000

The EHG is the largest and most heavily means-tested grant, and crucially, it's the only one available on new BTO flats. It's the workhorse of the stack.

How much, and the big 2024 boost

Since August 2024, the EHG ceiling was doubled from S$80,000 to S$120,000 for families (and from S$40,000 to S$60,000 for eligible singles). Here's a fact worth highlighting because it cuts through a lot of confusion: Budget 2026 did not increase this further. There was no new housing-grant giveaway this year. The "S$230K" figure is the existing stacked maximum that's been in place since late 2024 — not a fresh 2026 announcement.

The income ceiling and the sliding scale

To qualify for any EHG at all, your average gross monthly household income must be:

- ≤ S$9,000 for families

- ≤ S$4,500 for singles buying alone (or ≤ S$9,000 if buying with other singles or with parents)

The grant is means-tested in S$500 income bands — the lower your household income, the bigger the grant. It scales smoothly down from S$120,000 to S$0 as income rises to the S$9,000 ceiling. Here are some illustrative anchor points reported by 2026 guides:

EHG by Household Income Band (Family, illustrative)

A quick read of the anchor points:

- Household income ≤ S$1,500/mth → S$120,000 (the maximum)

- ~S$3,001–3,500/mth → ~S$90,000

- ~S$5,001–5,500/mth → ~S$55,000 — note the August 2024 doubling lifted this middle band sharply (reportedly from ~S$20K to ~S$55K)

- ~S$7,001–7,500/mth → ~S$25,000

- ~S$8,001–8,500/mth → ~S$10,000

- Above S$9,000/mth → S$0 (ineligible)

One important caveat: Secondary sources disagree on a few of the mid and upper bands — one worked example shows just S$5,000 EHG for a combined S$8,500 income, for instance. Treat the EHG as a declining S$500-band schedule and use these anchors as a guide only. For your exact number, always check the official HDB EHG e-calculator and confirm via your HFE letter. Don't budget off a blog table — including this one.

The other EHG conditions people forget

The income test isn't the only hurdle. To collect the EHG, you also need:

- Continuous employment: At least one applicant or occupier must have been employed for the 12 months before application, and still be working at the point of application.

- Lease coverage (for resale): The flat must have a remaining lease of at least 20 years, and the lease must cover the youngest buyer until age 95. If it doesn't, your EHG gets pro-rated downward.

That last point quietly disqualifies a lot of older flats from the full grant, so factor it in when you're shortlisting resale units with shorter leases.

Grant 2 — The Family Grant: The S$80,000 Nobody Talks About

If the EHG is the means-tested workhorse, the CPF Housing Grant — universally called the "Family Grant" — is the quietly generous one. It's resale-only, and it's the grant that lets even comfortable middle-income couples walk away with a serious sum.

| Flat size | Family Grant |

|---|---|

| 2- to 4-room resale | S$80,000 |

| 5-room or larger resale | S$50,000 |

Here's why it matters so much:

- The income ceiling is S$14,000/mth (rising to S$21,000 for extended or multi-generational families). That's far higher than the EHG's S$9,000 cap. The practical implication is huge: a middle-income couple earning, say, S$11,000 combined gets zero EHG but still pockets the full S$80,000 Family Grant.

- Smaller flats get more money. The S$80,000 tier applies to 2- to 4-room flats, while 5-room-and-larger units get S$50,000. It's a deliberate nudge toward right-sizing — and a genuine planning lever. A couple choosing a 4-room over a 5-room resale gains S$30,000 in grant and pays a lower purchase price.

- Singles get half. The "Singles Grant" version offers S$40,000 (2–4 room) or S$25,000 (5-room+), with a lower income ceiling of S$7,000.

The takeaway: the Family Grant is the reason the resale route is so powerful for middle earners. The EHG fades as you earn more, but the Family Grant holds steady almost all the way up to a S$14,000 household income.

Grant 3 — The Proximity Housing Grant: Up to S$30,000 for Living Near Mum and Dad

The Proximity Housing Grant (PHG) is the easiest top-up to capture, for one simple reason: it has no income ceiling at all. Every income tier qualifies, from a fresh graduate couple to a pair of high-earning professionals. It's resale-only, and it rewards you for staying close to family.

| Arrangement | Family | Singles |

|---|---|---|

| Living with parents/married child (same flat) | S$30,000 | S$15,000 |

| Living near (within 4 km) | S$20,000 | S$10,000 |

The conditions:

- If you're living together, the parents or married child must be co-applicants or essential occupiers on the flat.

- If you're living near, the parents or child must own and owner-occupy a property within 4 km of your new flat.

Because there's no income test, the PHG is the great equaliser. A high-earning couple who's blown past the EHG ceiling can still stack the Family Grant (S$80,000) and the PHG (S$30,000) for a combined S$110,000 — just for buying resale and living with or near their parents. That's the part the "you earn too much for grants" crowd tends to miss entirely.

Worked Scenarios: What's Actually on the Table for You

Theory is one thing. Let's run four realistic profiles to show how the stack behaves at different income levels — because the headline S$230K is only reachable by a specific household type.

Total Grant Stack by Buyer Scenario (S$)

Scenario A — Lower-income couple, maxing the stack

Combined income ~S$3,000/mth, buying a 4-room resale to live with parents.

- EHG ≈ S$90,000+ (low-income band)

- Family Grant S$80,000 (4-room)

- PHG S$30,000 (living together)

- Total: ~S$200,000–S$230,000

This is the household type that actually reaches the headline figure. Low enough income to catch a big EHG, resale to unlock the other two grants, and living with parents to max the PHG.

Scenario B — Median dual-income couple

Combined ~S$5,500/mth, 4-room resale near parents (within 4 km).

- EHG ~S$55,000 (middle band)

- Family Grant S$80,000

- PHG S$20,000 (living near)

- Total: ~S$155,000

A very common Singaporean profile — and still over S$150K in subsidy.

Scenario C — Higher-income couple, over the EHG ceiling

Combined ~S$10,000/mth, 5-room resale living with parents.

- EHG S$0 (over the S$9,000 ceiling)

- Family Grant S$50,000 (5-room)

- PHG S$30,000 (living together)

- Total: S$80,000

The lesson: even with zero EHG, S$80,000 is still on the table. Earning too much for the EHG doesn't mean earning too much for grants, full stop.

Scenario D — BTO first-timer couple

Combined ~S$5,000/mth, Standard 4-room BTO.

- EHG only, ~S$55,000–S$60,000

- No Family Grant, no PHG (these are resale-only)

- Total: ~S$57,000

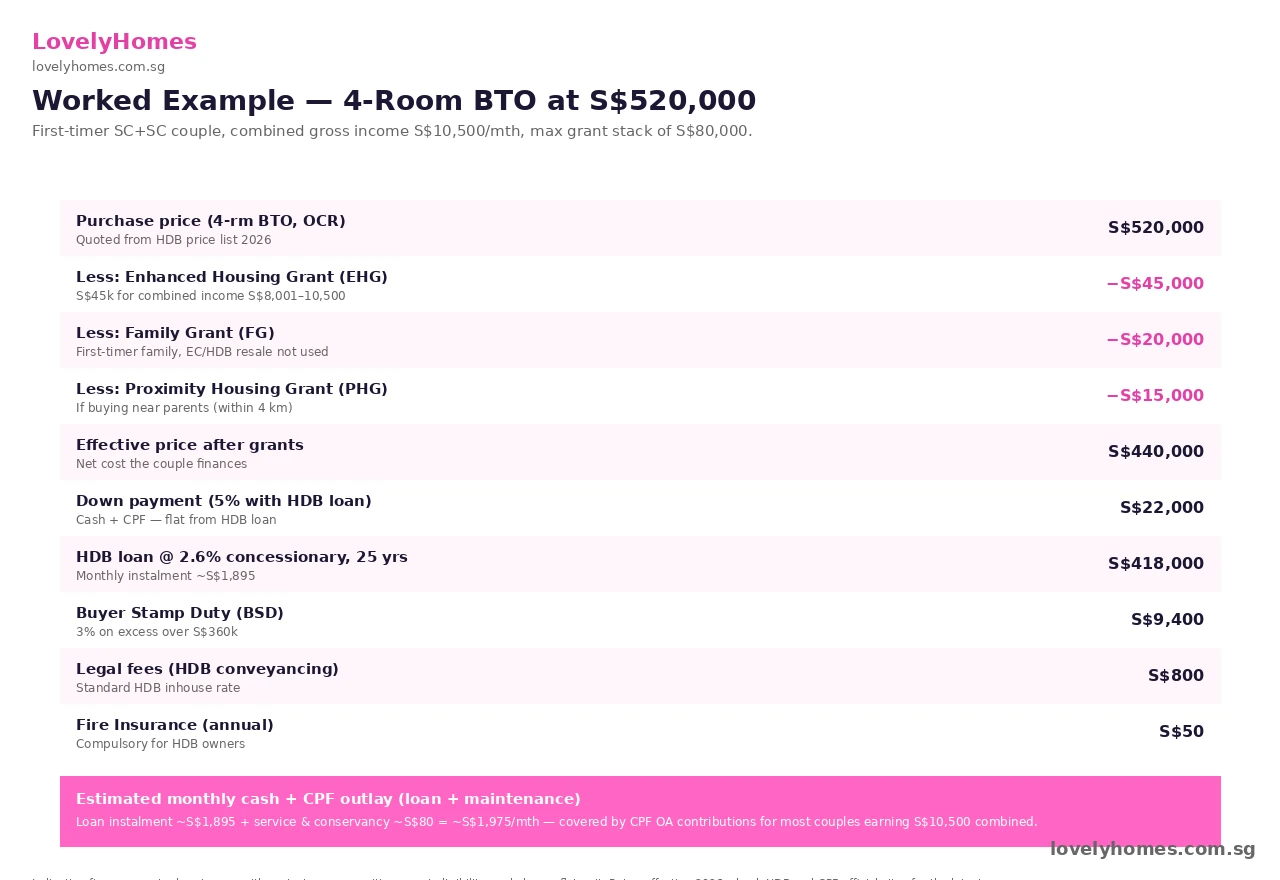

A reported June-2026 BTO example drives the point home: a couple earning S$8,500 combined buying a S$550,000 4-room got just S$5,000 EHG, trimming their lease-signing down-payment from S$53,000 to S$48,000. For higher-income BTO buyers, the grant is modest. The resale route is where the stacking magic happens.

Here's the decision logic that determines which scenario you fall into:

Budget 2026: The Cash-Flow Cushion Around the Grants

Grants are your capital subsidy — they shrink the upfront cost of the flat. But buying your first home is also the year your cash flow gets hammered: renovation, furnishing, stamp duty, legal fees, the lot. This is where Budget 2026 comes in.

Delivered by PM and Finance Minister Lawrence Wong on 12 February 2026, Budget 2026 contained no new housing-grant increases — but it layered on broad household relief that frees up cash exactly when a new homeowner needs it most. Here's the support calendar:

| Support measure | Amount | When |

|---|---|---|

| Cost-of-Living Special Payment (cash) | S$200–S$400 (one-off) | ~September 2026 |

| U-Save rebates (FY2026) | Up to S$570 (1.5× regular) | Apr, Jul, Oct 2026 & Jan 2027 |

| CDC Vouchers | S$500 per household | January 2027 |

A closer look at each:

- Cost-of-Living Special Payment: A one-off cash payout of S$200–S$400 to eligible Singaporeans aged 21+ in 2026, paid around September 2026 via bank transfer or PayNow-NRIC. Eligibility: assessable income ≤ S$100,000 and owning no more than one property. Around 2.4 million Singaporeans qualify. (Note: some blogs inflate this to "S$400–S$600" — the official MOF figure is S$200–S$400. Use the official range.)

- U-Save rebates: Eligible HDB households get 1.5× the regular U-Save rebate — up to S$570 for FY2026 — disbursed across April, July, October 2026 and January 2027, subject to owning no more than one property per household.

- CDC Vouchers: S$500 per household for around 1.4 million households in January 2027 — split between participating supermarkets and heartland merchants/hawkers.

These aren't housing grants, and you shouldn't confuse the two. But sequenced together, they form a useful first-year homeowner money timeline: your grant stack lands in your CPF at purchase, then the Special Payment cash arrives in September, U-Save rebates trickle in quarterly to offset utility bills in a freshly renovated flat, and the CDC Vouchers top things off in January 2027.

Why Grants Matter More in 2026: The Market Backdrop

Here's the tension that makes 2026 an interesting year to be a first-timer: grants help enormously, but resale prices are sitting near record highs — even as the market just hit a notable inflection point.

The HDB Resale Price Index fell 0.1% quarter-on-quarter in Q1 2026, to 203.4 (from 203.6 in Q4 2025). That's the first quarterly decline since Q2 2019 — seven years of uninterrupted gains, broken. To be clear, prices were still ~1.2% higher year-on-year, so this is a moderation, not a crash.

HDB Resale Price Index (recent quarters)

A few more data points worth knowing before you buy:

- 6,179 resale transactions in Q1 2026 — up 17.6% quarter-on-quarter, but 4.6% below Q1 2025's 6,590. Activity is healthy but not frothy.

- A record 412 million-dollar flats changed hands in Q1 2026 (up from 368 in Q4 2025): 190 were 4-room, 143 were 5-room, 78 were executive, and 1 was multi-generational. Around 90.8% were in mature estates like Toa Payoh, Bukit Merah, Queenstown and Ang Mo Kio. (ERA counts these slightly differently at 402, or 6.9% of deals — a minor methodology variance.)

- Affordability still holds for the median buyer. A reassuring 70.8% of Q1 2026 resale deals were below S$750,000, and 48.6% fell in the S$500K–S$750K band. Million-dollar flats grab headlines, but they're the exception.

That last point is the one to internalise. On a S$600,000 4-room resale flat, a S$150,000+ grant stack covers roughly 25% of the purchase price. That's a quarter of your home, subsidised.

The "stable-price, max-grant" window

Looking ahead, analysts at ERA and OrangeTee expect +2% to +5% price growth and around 26,000–27,000 transactions for 2026 — a "stable, moderating" market. The reason is supply: a record pipeline of roughly 102,000 units planned for 2026, including around 55,000 BTO units across 2025–2027.

The moderation is supply-led, which is a genuinely good thing for first-timers. It means you may be looking at a relatively rare window — stable prices and maximum grants at the same time — before the next up-leg in the cycle. Grants are at their post-2024 peak; prices have paused. For a first-time buyer, that combination doesn't come around often.

Policy Notes You Genuinely Need to Get Right

A few regulatory details can quietly reshape your math. Don't skip these.

- BTO is now Standard / Plus / Prime (since October 2024). Plus and Prime flats come with a 10-year Minimum Occupation Period, a subsidy-recovery clawback on resale (Prime is often 8–12%), and a S$14,000 income ceiling on future resale buyers. Grants still apply, but these restrictions change the long-term math. Don't treat all BTOs as equivalent.

- Eligibility to buy ≠ eligibility for the grant. You can qualify to buy a BTO with a household income up to S$14,000, yet earn too much for the EHG at anything over S$9,000. Two different thresholds.

- First-timer priority still applies in BTO ballots. Second-timer and mixed households face reduced grants and tighter rules.

- Grants are clawed back with accrued CPF interest when you sell. Again: it's not lost — it returns to your CPF retirement savings — but it's not a permanent cash gift either. Plan around it.

Food for Thought

Before you rush to the HDB e-calculator, sit with these questions:

-

Is the S$30,000 Proximity Housing Grant worth living within 4 km of your parents — for the rest of your MOP? The money is real, but so is the lifestyle trade-off. Where does the balance fall for you?

-

If you earn just over the S$9,000 EHG ceiling, would reducing a household income figure ever make financial sense — or is that a false economy once you account for the years of earnings you'd forgo? How do you weigh a one-time grant against a lifetime income curve?

-

Resale unlocks S$230K but costs more upfront; BTO is cheaper but caps you at the EHG. When you model the full picture — price, grants, wait time, and the new Plus/Prime restrictions — which route actually leaves you wealthier in ten years?

-

The HDB Resale Price Index just fell for the first time in seven years. Is a moderating market a signal to wait for lower prices, or a signal to lock in while grants are at their peak and supply is flooding in? What would change your answer?

-

Grants are credited to CPF, not cash, and must be refunded on sale. Does framing them as "free money" actually help you make a better decision — or does treating them as a forced retirement top-up lead to smarter planning?

The Bottom Line

For the right first-timer household — resale, living with or near parents, and within the income bands — S$230,000 in stacked CPF housing grants is entirely achievable, and Budget 2026's cash-flow support softens the most expensive year of your life on top of it. For everyone else, the stack still delivers somewhere between S$57,000 and S$155,000, which is hardly small change. The single highest-leverage move is understanding your exact number before you ever view a flat — get the HFE letter, run the official EHG calculator, and decide between resale and BTO with eyes open.