If you've been watching your mortgage statement with a mix of relief and confusion lately, you're not alone. The 3-month compounded SORA — the benchmark that powers most floating-rate home loans in Singapore — settled at 1.0807% on 15 May 2026, the lowest reading in roughly four years. That's nearly 200 basis points below the 3.03% peak set in early 2025, and it has triggered the most aggressive bank refinancing war Singapore has seen since the post-COVID years.

Fixed-rate packages now start from 1.35%. The cheapest floating packages are offering 3M SORA + 0.20–0.25% — an all-in rate of about 1.28–1.33%. And here's the catch: bank house views, led by UOB, expect SORA to climb back toward ~1.39% by Q4 2026. The window is open. It may not stay this way for long.

This guide breaks down exactly what's happening with Singapore mortgage rates in May 2026, how to math out whether refinancing makes sense for your specific loan, which banks are leading on price, and how to pick between locking in a fixed rate or riding the floating wave. If you're sitting on a legacy loan from the 2.5–3% era, the next 90 days may be the single most consequential financial decision you make this year.

How Singapore Got To 1.08% SORA

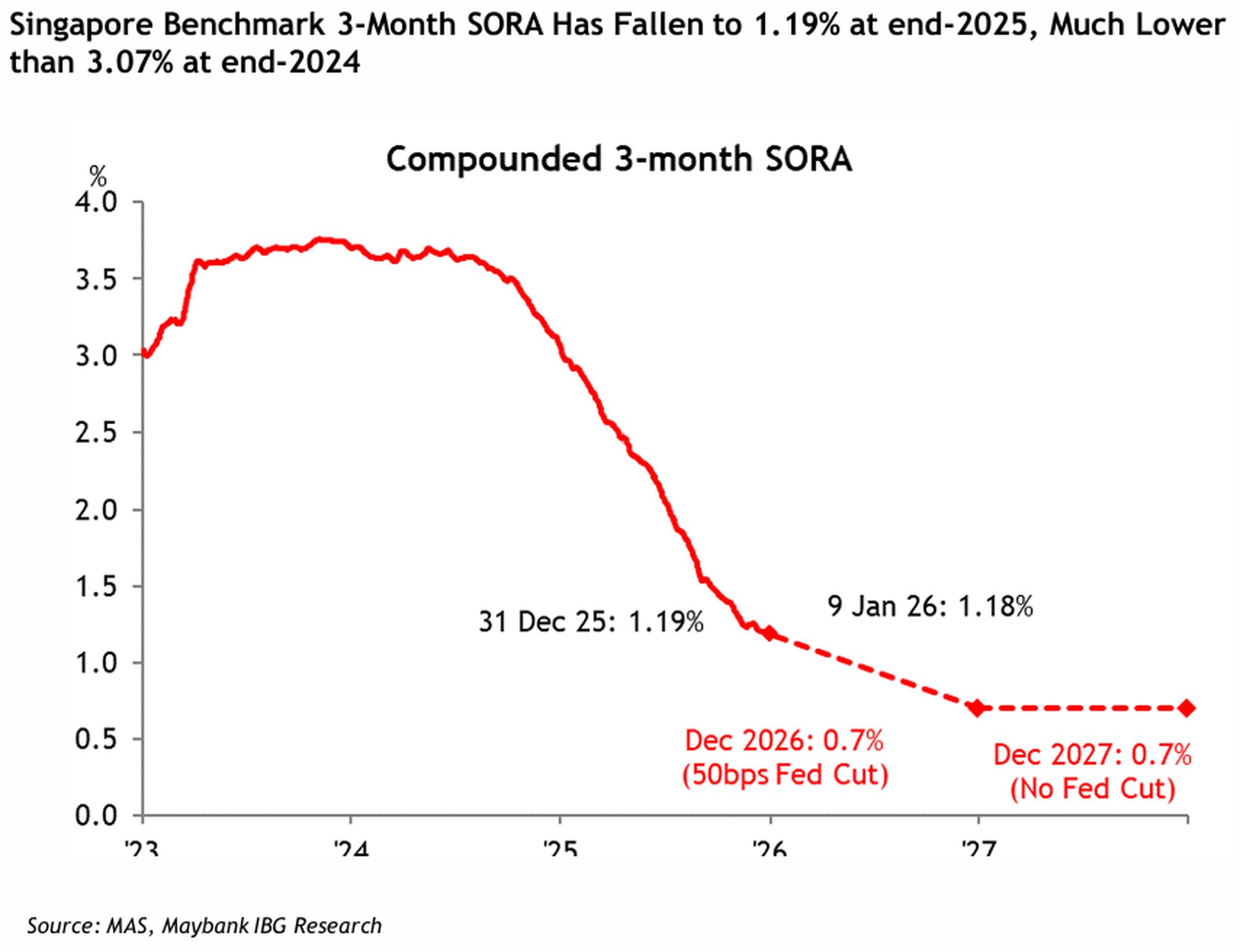

To understand why rates collapsed so quickly, it helps to recall where we just came from. SORA peaked at 3.03% in early 2025 as the Federal Reserve held US policy rates at multi-decade highs to fight post-pandemic inflation. Singapore, despite running its own SGD-based monetary policy through the NEER (Nominal Effective Exchange Rate) framework, imports US dollar funding costs through the FX swap market — meaning Fed policy heavily influences local interbank rates.

Once the Fed pivoted in late 2024 and began cutting, SORA followed almost mechanically. Over roughly 14 months, the index fell from 3.03% → 1.08%, a ~195 bps decline that translated directly into lower mortgage payments for every Singaporean on a floating-rate loan.

3-Month Compounded SORA Cycle (2025–2026)

The chart above shows the trajectory and the consensus forecast. Most of the fall is now behind us. Brokers like MortgageWise have stated bluntly: "1M and 3M SORA would certainly already be at the lowest point in this cycle at 1.00–1.10%."

That single sentence is the entire thesis of this article. If the floor is in, the asymmetry of locking in cheap money today is enormous — your downside is maybe 10–15 bps further fall, your upside protection is 50–100 bps if forecasts hold.

A Brief Note On What SORA Actually Is

SORA — the Singapore Overnight Rate Average — is the volume-weighted average rate of unsecured overnight interbank SGD borrowing transactions. The MAS publishes a daily reading, plus compounded 1-month, 3-month and 6-month averages that most home loans reference. Compounded SORA is a backward-looking, smoothed number — which is exactly why mortgages use it. It's much less spiky than the daily SORA print, and it gives borrowers a transparent, manipulation-resistant benchmark since SIBOR was retired.

For homeowners, the practical takeaway is simple: when you see "3M SORA + 0.25%" in a bank brochure, your effective rate this quarter is today's 3-month compounded SORA + 0.25%. Right now that's about 1.33% all-in.

The Refinancing Window: Why May–August 2026 Matters

Three forces are converging to create what brokers are quietly calling a "once-a-cycle" refinancing window:

- SORA is at or near its cyclical floor (1.08% spot, with consensus floor view at 1.00–1.10%)

- Bank pricing is the most aggressive it has been since 2021 — fixed packages from 1.35%, floating spreads compressed to 0.20–0.25%

- The MAS shifted to a tightening bias in April 2026, raising the SGD appreciation slope by ~50 bps to ~1% in response to oil and tariff-driven inflation pressures

That last point is critical and often missed in headline coverage. MAS tightening doesn't directly push SORA up — SGD strength is the lever, not SGD interest rates — but it narrows the SGD/USD rate differential, reducing the room for local money-market rates to keep falling even if the Fed cuts further.

In other words: the macro forces that pushed SORA down are losing steam, and new forces are starting to point the other way. The window is open precisely because we're at the inflection point — not because rates will keep falling.

The MAS April 2026 Decision In Plain English

On 14 April 2026, MAS surprised some economists by raising the slope of the S$NEER policy band. The trigger was a combination of:

- Oil and gas price shock from the US–Iran conflict and shipping disruptions through the Strait of Hormuz

- Core inflation forecast revised up to 1.5–2.5% (from the previous 1.0–2.0% range)

- Concern that tariff-driven import price pass-through could re-anchor inflation expectations

MAS explicitly said: "MAS Core Inflation will pick up and remain elevated over the next few quarters." For mortgage borrowers, this is a yellow flag — not a red one. SORA isn't suddenly heading back to 3%, but the comfortable consensus that rates will keep falling has been quietly retired.

Fixed vs Floating: The Math Is Closer Than Ever

The single most-asked question right now is: "Should I lock in fixed at 1.35%, or take the cheaper floating at 1.28%?" Let's do the math.

Today's Package Snapshot (May 2026, Indicative)

| Bank | Lowest 2-Yr Fixed | Floating (3M SORA + spread) | All-In Floating |

|---|---|---|---|

| DBS | ~1.65–1.70% | SORA + 0.40–0.80% | 1.48–1.88% |

| OCBC | ~1.60–1.65% | SORA + 0.35–0.75% | 1.43–1.83% |

| UOB | ~1.65–1.75% | SORA + 0.40–0.80% | 1.48–1.88% |

| POSB HDB (3-yr fixed) | 1.70% | — | — |

| SCB (refi target) | From 1.35% | SORA + 0.20–0.25% | 1.28–1.33% |

| Broker-sourced best | 1.35% | SORA + 0.20% | 1.28% |

A few important things to notice from this snapshot:

- The spread between best fixed and best floating is roughly 5–10 basis points. That's historically tiny — in 2022–2023 the gap was often 50–80 bps.

- Local banks (DBS/OCBC/UOB) are typically 20–30 bps off the broker-sourced best. Walking into a branch and accepting the headline rate is almost always more expensive than getting two or three quotes through a broker.

- SCB and foreign-bank refi specials are setting the price floor, with local banks then matching selectively for high-quality refinancers.

The Break-Even Question

If you take floating at 1.33% all-in today, what's the SORA path that makes fixed at 1.35% the better deal?

The simple answer: fixed wins as soon as the average SORA over your 2-year lock-in exceeds about 1.10%. Given spot SORA is already 1.08% and UOB forecasts it climbing to 1.39% by year-end, the average over the next 24 months is almost certainly going to be higher than 1.10%.

Projected All-In Mortgage Rate vs SORA Path

In other words, the floating package only "wins" if SORA stays remarkably close to its current floor for most of the next two years. That's possible — but it requires the Fed to keep cutting, MAS to reverse its April tightening, and inflation to stay subdued. None of those are base cases.

The MortgageWise View: Pay For Optionality, Not Just The Lowest Rate

Multiple brokers, MortgageWise most prominently, have argued that the real prize right now isn't squeezing the last 5 bps out of a floating package. It's the protection a fixed lock gives you against a 2027 inflation rebound.

Their stress case: tariff-driven inflation in mid-2026 forces MAS or the Fed back into hiking mode by early 2027. SORA spikes 50–100 bps over six months. A floating borrower with no lock-in gets repriced; a fixed borrower at 1.35% sleeps fine until 2028.

The cost of that insurance? Roughly 5–10 bps of headline rate. For a S$1M loan, that's about S$50–80 per month of "insurance premium." Most professionals will tell you that's the cheapest financial hedge available in Singapore right now.

Worked Examples: What Refinancing Actually Saves

Numbers are abstract until they're attached to a real loan. Let's walk through two common scenarios.

Scenario 1: Private Condo Owner On Legacy 2.50% Package

- Loan: S$1,000,000 outstanding

- Tenure remaining: 25 years

- Current rate: 2.50% (a typical 2024-era refinance package)

- New rate: 1.35% fixed (2-yr)

| Metric | Current | After Refi | Difference |

|---|---|---|---|

| Monthly instalment | ~S$4,486 | ~S$3,932 | –S$554 / month |

| Annual saving | — | — | ~S$6,648 |

| 2-yr saving (lock-in period) | — | — | ~S$13,296 |

| Refi cost (post-subsidy) | — | S$0–S$1,500 | — |

| Break-even | — | — | Instant to 3 months |

If your loan is in this range and you're past your lock-in, refinancing is functionally free money.

Scenario 2: HDB Owner On 2.60% Concessionary Loan

- Loan: S$500,000 outstanding

- Tenure remaining: 20 years

- Current rate: 2.60% HDB concessionary (CPF OA + 0.10%)

- New rate: 1.55% bank fixed (typical HDB refi promo)

| Metric | Current | After Refi | Difference |

|---|---|---|---|

| Monthly instalment | ~S$2,672 | ~S$2,433 | –S$239 / month |

| Annual saving | — | — | ~S$2,868 |

| 5-yr saving | — | — | ~S$14,340 |

The HDB case carries one giant asterisk we'll cover in detail later: the move from HDB to bank is irreversible. You cannot move back. For some homeowners — especially those who might downgrade later, or who value the predictability of a stable 2.60% across the cycle — staying put can still be the right call even though the bank rate is cheaper today.

Monthly Savings From Refinancing (S$)

The savings scale linearly with loan size. For a S$1.5M loan, you're looking at roughly S$10,000 a year in additional cash flow — enough to fully fund a CPF SA top-up, an SRS contribution, or just compound in a HYSA.

The Refinancing Cost Stack: What You Actually Pay

Many homeowners hesitate to refinance because they overestimate the cost. Here's what's actually on the bill in 2026:

- Legal fees: S$2,000–S$3,000 (sometimes up to S$3,500 for complex cases)

- Valuation fee: S$200–S$500

- Bank cash rebate / subsidy: S$2,000–S$3,500

- Net out-of-pocket: typically S$0–S$1,500

The subsidy thresholds matter:

- HDB refinance: loan must usually be ≥ S$300,000 to qualify for full legal subsidy

- Private refinance: loan must usually be ≥ S$400,000 for full subsidy

If you're below those thresholds, the math gets trickier. A S$200k HDB refinance with no subsidy might cost ~S$2,500 in legal + valuation, which on a 50 bps saving works out to about 18 months of break-even. Still worth doing, but no longer a no-brainer.

Repricing vs Refinancing

There's a third option that gets overlooked: repricing, which is the same-bank version of refinancing. It's faster (usually 1–2 months), free, and skips the legal/valuation circus entirely.

The trade-off: repricing rates are typically 10–25 bps worse than the best open-market refinancing rate, because your existing bank knows the friction cost of switching is real.

Rule of thumb: if your outstanding loan is under S$150,000, repricing usually beats refinancing on a net basis. Above that, the open-market rate advantage typically wins.

The Refinancing Decision Tree

The flowchart above captures the decision tree most brokers walk borrowers through. Three branches matter most:

- Lock-in status decides whether you can act at all (clawback is 1.5% of outstanding within lock)

- Loan size decides whether refinancing or repricing is more efficient

- Holding horizon decides fixed vs floating

The HDB Concessionary Loan Question

The HDB concessionary loan at 2.60% (CPF Ordinary Account rate + 0.10%) is the elephant in the room for HDB owners. It has stayed at 2.60% throughout the entire SORA cycle — meaning the gap between HDB and the best bank fixed rate has blown out to roughly 125 basis points (1.55% vs 2.60%).

For a S$500k HDB loan, that 125 bps gap is about S$240/month or ~S$2,900/year — meaningful, real money.

So why doesn't every HDB owner refinance? Three reasons:

- Irreversibility: Once you move from HDB to a bank loan, HDB will not grant the concessionary loan again on the same flat. If rates spike to 4% in 2028, you cannot move back to 2.60%.

- Future BTO eligibility: Refinancing your existing HDB loan does not affect future BTO eligibility per se, but it does affect your CPF balance dynamics and household debt picture.

- Stability premium: 2.60% is fixed at CPF OA + 0.10% by formula. It cannot suddenly become 4%. Bank rates, even on a 2-yr fixed, will reprice when the lock-in ends.

The MortgageWise/DollarBack consensus position: if your loan is ≥ S$300k, you have no plan to downgrade in the next 5+ years, and you can comfortably absorb a worst-case repricing in 2028 to ~3%, switching to a bank loan today is rational. If any of those don't apply, the certainty of HDB at 2.60% is worth more than the headline saving.

Bank-By-Bank: Who Is Leading On Price?

Here's what the May 2026 market looks like across the major players:

Local Banks

- DBS: Historically the price leader, currently sitting in the middle of the pack on fixed (1.65–1.70%) but aggressive on its 2-yr lock-in floating packages with rebates targeted at high-loan-quantum refinancers.

- OCBC: Often the lowest local-bank headline on fixed (1.60–1.65%). Strongest on HDB refinancing promos with bundled cash rebates.

- UOB: Slightly higher headline rates (1.65–1.75%) but the most generous on relationship banking — wealth-tier customers can often negotiate 10–20 bps off published rates.

- POSB: The HDB specialist with a 3-yr fixed at 1.70%, attractive for borrowers who want longer rate certainty without paying a big premium.

Foreign Banks

- SCB (Standard Chartered): The aggressor of this cycle. Refinancing-targeted packages are typically 5–15 bps below local banks, and SCB is the bank most commonly quoted at the 1.35% fixed headline through broker channels.

- HSBC, Citibank, Maybank: Selectively competitive, often through private-banking relationships rather than mass-market pricing.

The practical implication: never accept the first quote from your existing bank. The published rate is the worst rate. Brokers and competitive shopping typically save another 10–30 bps on top of whatever the bank initially offers.

The Singapore Property Market Backdrop

Refinancing decisions don't happen in isolation — they happen against a property market that's still resilient despite the rate cycle. The Q1 2026 picture:

| Indicator | Q1 2026 Reading |

|---|---|

| URA Private Residential Index | +0.9% q-o-q (6th consecutive quarter of growth) |

| Non-landed | +1.3% |

| Landed | –1.8% |

| OCR | +2.2% |

| RCR | +0.8% |

| CCR | +0.6% |

| Transactions | 4,041 units (–39.7% q-o-q) |

| Resale median (private) | S$1,763 psf |

| RCR median | S$2,672 psf |

| CCR notable: River Modern | 92% take-up, S$3,216 psf median |

ERA's commentary attributed Q1 demand resilience to "lower interest rates and rising HDB prices have boosted buyers' financial ability." Translation: falling SORA has been a tailwind for property prices, which is why the OCR — where most upgraders shop — is leading the gain.

The transaction volume drop (–39.7% q-o-q) looks alarming but is mostly mechanical: Q4 2025 had multiple major launches, Q1 2026 had only six. Pipeline for Q2–Q4 2026 is 8,892 units across 20 projects, OCR-weighted — supply is coming.

For refinancers, the property-market context matters in one specific way: valuation. When you refinance, the bank will revalue your property. In a rising market, this often unlocks additional equity that can be used to negotiate better rates or extract cash. In flat or falling markets, a lower valuation can shrink your loan-to-value (LTV) and trigger top-ups. May 2026 is firmly in the "rising valuation" camp for most segments — another small tailwind for refinancers.

The Refinancing Checklist

Here's the operational checklist most brokers run through with clients. Work through it in order:

-

Check your lock-in expiry date. Most bank packages have a 2-year lock-in with a 1.5% clawback on the outstanding balance if exited early. Act roughly 3 months before expiry — that's the standard window for booking the next package without clawback.

-

Pull your current loan letter and statement. Confirm: outstanding balance, remaining tenure, current effective rate, and any prepayment penalties.

-

Get quotes from at least 3 banks plus 1 broker. Local banks (DBS, OCBC, UOB), one foreign bank (SCB or HSBC), and one broker (MortgageWise, Redbrick, DollarBack). Brokers typically beat walk-in rates by 5–10 bps because they aggregate volume.

-

Confirm subsidy thresholds. Loan must usually be ≥ S$300k for HDB or ≥ S$400k for private to qualify for full legal subsidy. Below the threshold, model the net cost.

-

Run break-even. Formula: (Legal + Valuation – Rebate) ÷ Monthly Saving = Months to payback. Anything under 12 months is a clear win; 12–24 months is acceptable if you're holding the property long; above 24 months suggests repricing instead.

-

Stress-test the loan. Model two scenarios: (a) SORA at UOB year-end forecast of 1.39%, and (b) SORA back at 2.00% (the inflation-rebound case). If your instalment is uncomfortable in either, lean fixed.

-

Decide repricing vs refinancing. Repricing is faster, free, and same-bank. Refinancing usually delivers a better rate but takes 2–3 months and involves paperwork. For loans under S$150k, repricing usually wins on net basis.

-

Confirm no prepayment plans in next 24 months. If you might sell, downgrade, or fully repay within the lock-in window, the clawback (1.5% of outstanding) erodes the saving fast. Either choose a no-lock-in floating package, or push the refi back.

Lock-In vs Flexibility: A Framework

The right answer depends on your specific situation. Here's a quick framework:

| Your Situation | Recommended Package |

|---|---|

| Holding property ≥ 3 years, want payment certainty | 2-yr fixed at 1.35–1.65% |

| Plan to sell or fully repay within 2 years | Floating with no lock-in (SORA + ~0.40%) |

| Expect SORA to rise faster than 1.39% by year-end | 3-yr fixed if available (1.55–1.70%) |

| Confident SORA stays sub-1.20% all of 2026 | Floating at SORA + 0.20–0.25% |

| HDB owner on 2.60%, loan ≥ S$300k, no downgrade plans | Refinance to bank, accept irreversibility |

| HDB owner with small balance or risk-averse | Stay on HDB loan at 2.60% |

| Investor on multiple properties | Mix — fixed on long-hold, floating on near-sale |

The repeated theme: the 5–10 bps gap between fixed and floating is small compared to the regret cost of being trapped in a floating package if SORA spikes back to 2%+ in 2027.

Risks To The Bullish Refinancing Narrative

No analysis is complete without the downside cases. Here are the four risks worth taking seriously:

-

Oil shock persistence: If Strait of Hormuz disruption extends and oil stays elevated through 2026, MAS could tighten further. SGD strengthens, but local liquidity tightens — SORA could climb faster than the 1.39% forecast.

-

Fed surprise: If the Fed pauses cuts in H2 2026 (because US inflation re-accelerates), USD funding costs rise and SORA gets pulled up mechanically through the FX swap channel.

-

Tariff inflation in mid-2026: MortgageWise's scenario. Tariff pass-through on imported goods could compress the floating-rate window to weeks, not months. Fixed becomes a much better deal much faster than the consensus expects.

-

Downside risk (cushion case): A risk-off event — China credit stress, Taiwan tensions, broad equity selloff — could briefly push SORA back below 1.00%. But the asymmetry of upside (potentially 100+ bps higher) vs downside (maybe 10–20 bps lower) from current levels strongly favours locking in.

Food For Thought

A few questions worth sitting with before you make a decision:

-

What does your 24-month plan look like? If there's any meaningful chance of selling, downgrading, or doing major capital expenditure in the next two years, a lock-in package is a different decision than for someone planning to hold for a decade.

-

How much volatility can your monthly cash flow absorb? If a SORA spike to 2.5% would mean genuine household budget stress — not just discomfort — then the 5–10 bps premium for fixed is the cheapest insurance you'll ever buy.

-

Are you optimising for the lowest headline rate, or the best risk-adjusted outcome? These are different problems. The headline-rate winner today is floating at 1.28%. The risk-adjusted winner for most households is fixed at 1.35%.

-

If you're on an HDB loan at 2.60%, what is the value of optionality to you? The 2.60% is forever (well, indefinitely). The bank rate is for 2 years. Are you paying ~S$240/month for the right to never be repriced above 3%?

-

When was the last time you actually shopped your mortgage? Most homeowners reprice or refinance once every 2–3 years out of inertia. With rates having moved 200 bps, the cost of inertia in 2026 is materially higher than usual.

Conclusion

The 2026 refinancing window is real, it's measurable, and for most homeowners with loans above S$300k, the math is one-sided. SORA at 1.08% is a near-cyclical floor; fixed packages from 1.35% are extraordinary by historical standards; and the policy + macro setup (MAS tightening, tariff inflation risk, narrowing rate differentials) all argues for locking in now rather than waiting for a deeper bottom that probably isn't coming.

The single highest-leverage action a Singapore homeowner can take this quarter is to:

- Pull your current loan letter

- Get three competitive quotes (at least one through a broker)

- Run the break-even number on a calculator

- Decide between fixed and floating based on your holding horizon, not the headline rate

If you're past your lock-in, the cost of inaction is roughly S$500–S$800 per month of foregone savings on a typical S$1M condo loan. That's real money, every month, indefinitely — until SORA rises again and the window closes.