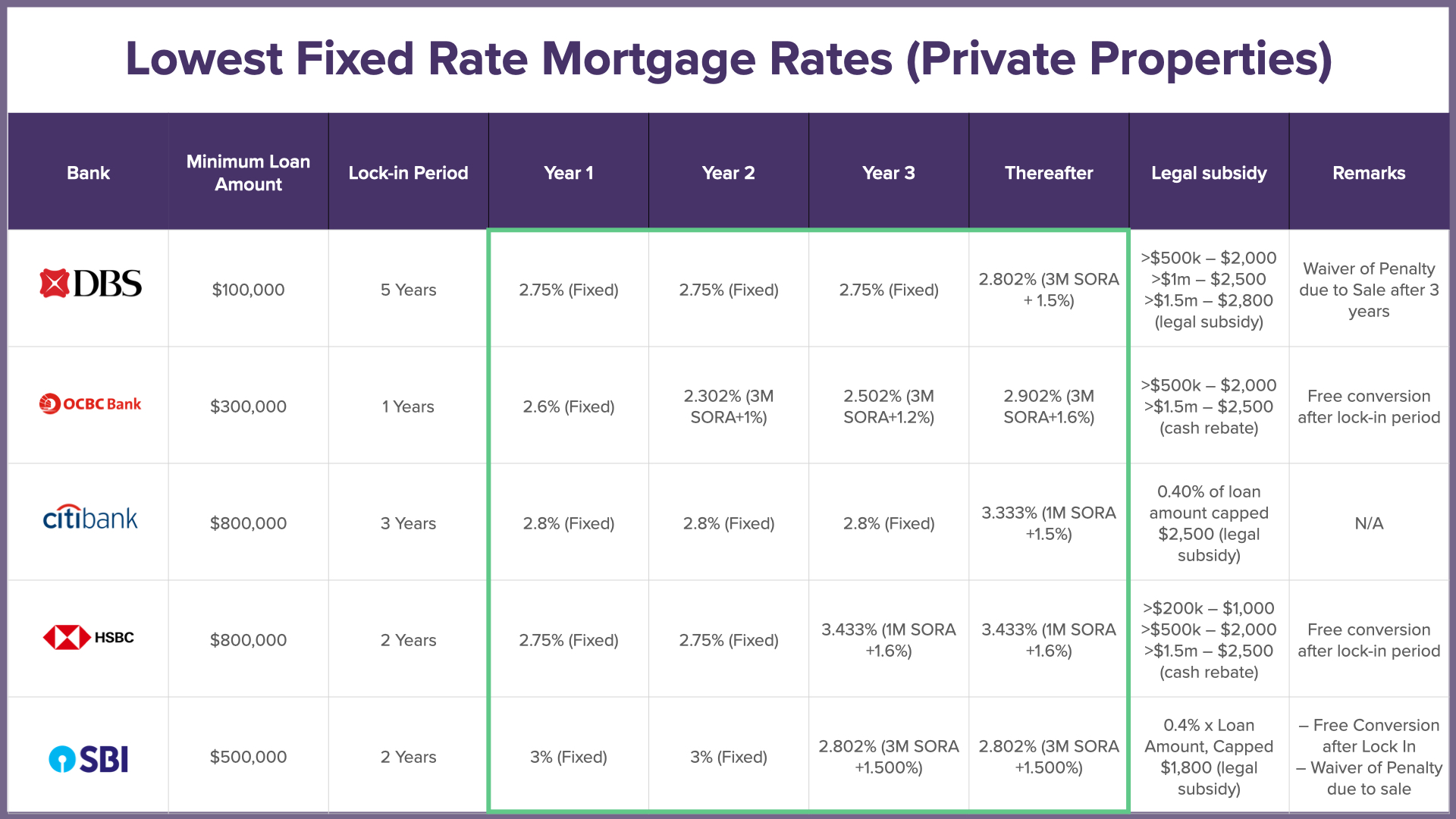

The moment many Singaporean homeowners have been waiting for has finally arrived. After nearly two years of elevated borrowing costs that squeezed budgets and cooled property enthusiasm, DBS has fired the starting gun on a new era of sub-3% mortgage rates with its 2.98% fixed-rate offering. This isn't just a marketing headline—it's a fundamental reset of the financial calculus for anyone with a property loan in Singapore.

Whether you're a first-time buyer calculating your maximum loan quantum, an existing homeowner wondering if you should refinance, or an investor reassessing your portfolio leverage, this shift demands immediate attention. The window for securing historically attractive rates may be narrower than you think, and the decisions you make in the coming months could save—or cost—you tens of thousands of dollars over your loan tenure.

In this comprehensive guide, we'll break down exactly who qualifies for these sub-3% rates, how to calculate your break-even point for refinancing, what lock-in periods really mean for your flexibility, and how competitor banks like OCBC and UOB are likely to respond. More importantly, we'll model different scenarios for 2024-2025 rate trajectories to help you time your move optimally.

The Sub-3% Era: Understanding What Just Changed

From Peak Pain to Present Opportunity

To appreciate the significance of DBS's 2.98% fixed rate, we need to understand where we've come from. In 2022-2023, Singapore mortgage rates peaked at 3.0% to 3.5% as global central banks aggressively hiked rates to combat inflation. For a typical $1 million loan over 25 years, that rate difference translates to meaningful monthly savings.

Singapore Mortgage Rate Evolution (2022-2025)

The chart above illustrates the steady decline in mortgage rates, with DBS's 2.98% offering representing a psychological breakthrough below the 3% threshold. This matters because 3% has historically served as a mental anchor for Singaporean borrowers—rates above this level trigger caution, while rates below it stimulate activity.

Why Rates Are Falling: The SORA Connection

Singapore's mortgage rates don't move in isolation. They're tightly coupled to the Singapore Overnight Rate Average (SORA), which has replaced the Singapore Interbank Offered Rate (SIBOR) as the primary benchmark for floating-rate home loans. SORA reflects the actual cost of overnight borrowing between banks in Singapore and is heavily influenced by U.S. Federal Reserve policy.

According to market forecasts, the 3-month SORA is projected to decline from approximately 2.9% currently to a range of 2.2%-2.6% by the end of 2025, potentially bottoming out near 1% around Q2 2026 before modestly recovering to approximately 1.39% by year-end 2026. This anticipated trajectory creates a strategic window for borrowers to secure favorable rates.

SORA Forecast Trajectory (2024-2026)

What DBS's 2.98% Actually Means

DBS's headline 2.98% fixed rate isn't a one-size-fits-all offering. Here's what you need to know:

| Feature | Typical Terms |

|---|---|

| Fixed Rate Period | 2-3 years (varies by package) |

| Lock-in Period | Usually matches fixed period |

| Minimum Loan Amount | Typically $100,000-$300,000 |

| Early Redemption Penalty | 0.75% - 1.50% of outstanding loan |

| Partial Prepayment | Often allowed with conditions |

| Legal Fee Subsidy | May be available for refinancing |

The key differentiator for DBS is their waiver of penalties upon property sale during the lock-in period—a feature that provides valuable flexibility if your circumstances change. Some packages also include complimentary partial prepayments, allowing you to reduce your principal without penalty.

Who Qualifies for Sub-3% Rates: The Eligibility Reality Check

The Standard Requirements

Securing DBS's 2.98% rate—or any competitive mortgage package—requires meeting established banking criteria. While specific requirements vary, expect to demonstrate:

- Stable Employment: Minimum 2 years with current employer for salaried workers; 2-3 years of consistent income for self-employed professionals

- Income Adequacy: Your monthly debt obligations, including the new mortgage, must fall within Total Debt Servicing Ratio (TDSR) limits—currently 55% of gross monthly income

- Clean Credit History: No recent defaults, bankruptcies, or significant delinquencies

- Appropriate Loan-to-Value (LTV): For your first property loan, you can borrow up to 75% of property value; subsequent loans face lower limits (45% or 35% depending on property type and existing loans)

The Hidden Filters

Beyond these standard requirements, banks apply additional screening that can affect your eligibility for the best rates:

| Factor | Impact on Rate Eligibility |

|---|---|

| Property Type | Private condos and landed properties often qualify for better rates than HDB flats |

| Loan Size | Larger loans ($500K+) typically unlock preferential pricing |

| Existing Relationship | DBS customers with significant deposits/investments may receive priority |

| Age + Loan Tenure | Combined cannot exceed 65 years (or 70 with enhanced criteria) |

| Property Location | Prime districts may be viewed more favorably |

The TDSR Calculation That Matters Most

Here's where many applicants stumble. The TDSR calculation includes:

- Your proposed mortgage payment

- All existing debt obligations (car loans, credit cards, personal loans, other property loans)

- A stress-tested buffer—banks must apply a higher interest rate (typically 3-4% above the offered rate) to ensure you can handle rate increases

Example TDSR Calculation:

| Monthly Income & Obligations | Amount |

|---|---|

| Gross Monthly Income | $10,000 |

| Existing Car Loan | $800 |

| Credit Card Minimums | $200 |

| Proposed Mortgage at 2.98% | $3,500 |

| Total Monthly Obligations | $4,500 |

| TDSR | 45% ✓ (Below 55% limit) |

At 45% TDSR, this borrower qualifies. But if the stress test at 6.98% pushes obligations above 55%, the loan amount may be reduced or declined.

Lock-In Periods: The Flexibility Trade-Off Explained

What You're Really Committing To

Fixed-rate mortgages universally come with lock-in periods—typically 2-3 years, though some banks offer 5-year options. During this period, you face penalties for:

- Full loan redemption (selling your property)

- Refinancing with another bank

- Making prepayments beyond allowed limits

The Penalty Structure Decoded

| Scenario | Typical Penalty |

|---|---|

| Early full redemption during lock-in | 0.75% - 1.50% of outstanding loan amount |

| Partial prepayment exceeding allowance | 1.00% - 1.50% of excess prepayment amount |

| Refinancing before lock-in expiry | Same as early redemption penalty |

| Failure to give 3-month notice | Additional administrative fees |

Critical detail: Most banks require 3 months' written notice before any refinancing or full settlement. Miss this window, and you may face penalties beyond the standard lock-in charges.

DBS's Competitive Advantage: Penalty Waivers

Where DBS differentiates itself is through selective penalty waivers:

- Property sale waiver: If you sell your property during the lock-in period, DBS typically waives the early redemption penalty

- Partial prepayment allowances: Some packages permit penalty-free partial prepayments up to a specified percentage annually

This flexibility is valuable. Consider: if you secure a 2.98% rate with a 3-year lock-in but receive an attractive job offer overseas in year 2, the property sale waiver could save you thousands in penalties.

The 5-Year Lock-In Gamble

Some borrowers are tempted by 5-year fixed rates, which may offer slightly lower rates (perhaps 2.85-2.90%). The trade-off:

Pros:

- Extended payment certainty

- Potentially lower rate

- Protection against rate volatility

Cons:

- Reduced flexibility for 5 years

- Higher penalties if circumstances change

- Opportunity cost if rates fall further

For most borrowers in the current environment, 2-3 year lock-ins offer the optimal balance of rate security and future flexibility.

Break-Even Calculations: The Math That Determines Your Move

When Refinancing Makes Financial Sense

If you currently have a mortgage, the critical question isn't whether 2.98% sounds attractive—it's whether refinancing to this rate will save you money after all costs are accounted for.

The Complete Cost Inventory

| Cost Category | Typical Amount | Notes |

|---|---|---|

| Early Redemption Penalty (if in lock-in) | 0.75% - 1.50% of outstanding loan | Often the largest cost |

| Legal Fees | $2,000 - $3,000 | May be partially subsidized by new bank |

| Valuation Fees | $300 - $500 | Required by new lender |

| Fire Insurance | $100 - $300 | May need to switch insurers |

| Clawback of Previous Subsidies | Variable | If you refinanced recently and received cash rebates |

Real-World Break-Even Scenario

Let's work through a concrete example:

Current Situation:

- Outstanding loan: $800,000

- Current rate: 3.6% (fixed, 1 year remaining on lock-in)

- Remaining tenure: 24 years

- Monthly payment: $3,998

Refinancing to DBS 2.98%:

- New rate: 2.98% (3-year fixed)

- New tenure: 24 years (maintained)

- New monthly payment: $3,520

- Monthly savings: $478

Refinancing Costs:

- Early redemption penalty (1.5%): $12,000

- Legal fees (after $2,000 subsidy): $800

- Valuation fee: $400

- Total costs: $13,200

Break-even calculation: $13,200 ÷ $478 = 27.6 months (2.3 years)

Decision framework:

- If you plan to hold the property and loan for more than 2.5 years, refinancing makes sense

- If you might sell within 2 years, the costs outweigh the benefits

- Consider that after the 3-year fixed period, you'll need to refinance again—factor in future costs

The "No Lock-In" Opportunity Window

If your current loan has exited its lock-in period, the math becomes dramatically more favorable:

| Scenario | With Lock-in Penalty | Without Lock-in Penalty |

|---|---|---|

| Total refinancing costs | $13,200 | $1,200 |

| Monthly savings | $478 | $478 |

| Break-even period | 27.6 months | 2.5 months |

Bottom line: If you're out of lock-in, refinancing to sub-3% rates is almost certainly advantageous.

Advanced Consideration: Interest Savings vs. Cash Flow

Some borrowers focus narrowly on monthly payment reduction, but the total interest saved over your loan tenure is equally important:

| Metric | Current Loan (3.6%) | New Loan (2.98%) | Difference |

|---|---|---|---|

| Monthly payment | $3,998 | $3,520 | $478 |

| Total interest over 24 years | $351,424 | $213,760 | $137,664 |

Even after accounting for refinancing costs, the total interest savings of approximately $137,000 represent substantial wealth preservation.

The Competitive Landscape: DBS vs. OCBC vs. UOB

How Competitors Are Responding

DBS's 2.98% move has triggered competitive responses across Singapore's banking sector. While specific rates fluctuate weekly, here's the strategic positioning:

| Bank | Fixed Rate Positioning | Notable Features |

|---|---|---|

| DBS | 2.98% (2-3 year fixed) | Penalty waiver on property sale; ecosystem integration |

| OCBC | Expected 2.95-3.05% range | Competitive for existing customers; flexible packages |

| UOB | Expected 2.98-3.10% range | Strong valuation for prime properties; relationship pricing |

OCBC's Likely Response Strategy

OCBC has historically been aggressive in matching or slightly undercutting DBS on headline rates. Market observers anticipate:

- Rate matching at 2.98% for comparable tenures

- Enhanced cashback offers to offset refinancing costs

- Priority processing for existing OCBC customers

- Bundled product incentives (credit cards, insurance, investments)

UOB's Positioning

UOB may take a slightly different approach:

- Slightly higher headline rates (3.00-3.10%) but with more flexible terms

- Longer fixed-rate options (4-5 years) for rate-certain seekers

- Stronger focus on high-value loans ($1M+) with preferential pricing

- Integration with UOB property ecosystem (valuation, legal, insurance)

The Floating Rate Alternative

While fixed rates grab headlines, floating-rate packages deserve consideration—especially given SORA's projected decline:

| Package Type | Current Rate | Pros | Cons |

|---|---|---|---|

| 3-Month SORA + Spread | ~3.0-3.2% | Potential savings if SORA falls; no lock-in | Payment uncertainty; rates could rise |

| 6-Month SORA + Spread | ~3.1-3.3% | Slightly more stability than 3-month | Less responsive to rate drops |

| 1-Month Compounded SORA | ~2.9-3.1% | Most responsive to market changes | Highest volatility |

The floating rate gamble: If SORA falls to 1.5% by mid-2026 as forecasted, a floating-rate borrower at SORA + 1.0% could see effective rates of 2.5%—below even today's fixed rates. But if inflation resurges and rates climb, floating-rate borrowers face payment increases.

Fixed vs. Floating: Decision Framework

Scenario Modeling: 2024-2025 Rate Trajectories and Timing

Three Possible Futures

No one can predict interest rates with certainty, but we can model scenarios to inform your decision-making:

Scenario A: "Soft Landing" (Most Likely - 50% Probability)

- U.S. Federal Reserve implements 2-3 rate cuts in 2024-2025

- Singapore 3-month SORA declines to 2.2-2.6% by end-2025

- Mortgage fixed rates stabilize around 2.75-3.00%

- Optimal strategy: Lock in 2.98% now or wait 3-6 months for potentially 2.85-2.90%

Scenario B: "Aggressive Easing" (30% Probability)

- Global recession fears trigger 4-5 Fed rate cuts

- SORA falls rapidly to 1.5-2.0% by mid-2025

- Fixed mortgage rates drop to 2.50-2.75%

- Optimal strategy: Choose floating rate now, refinance to fixed when rates bottom

Scenario C: "Inflation Resurgence" (20% Probability)

- Inflation proves persistent; Fed holds or hikes

- SORA remains elevated at 2.8-3.2%

- Fixed rates climb back above 3.2%

- Optimal strategy: Lock in 2.98% immediately for certainty

Timing Strategies by Borrower Profile

| Profile | Recommended Timing | Rationale |

|---|---|---|

| First-time buyer, urgent need | Act now at 2.98% | Don't time the market for your primary residence |

| First-time buyer, flexible timeline | Monitor for 2-3 months | May capture slightly better rates; risk missing window |

| Refinancing, out of lock-in | Immediate action | No downside to securing sub-3% rate |

| Refinancing, in lock-in | Calculate break-even | If break-even < 18 months, consider paying penalty |

| Investor with multiple properties | Stagger refinancings | Don't put all loans on same renewal cycle |

The "Wait vs. Act" Calculator

Here's a simplified framework for the timing dilemma:

If you WAIT 6 months:

- Potential rate improvement: 0.10-0.20% (Scenario A/B)

- Potential rate deterioration: 0.20-0.40% (Scenario C)

- 6 months of higher payments on current loan: $X

If you ACT NOW at 2.98%:

- Certainty of sub-3% rate locked

- Immediate monthly savings begin

- Protection against Scenario C

For most risk-averse borrowers, the certainty of 2.98% outweighs the potential benefit of waiting for marginally better rates.

Property Market Context: What Sub-3% Rates Mean for Singapore Real Estate

Market Resilience Despite Rate Volatility

Singapore's private residential property market has demonstrated remarkable resilience through the rate hiking cycle. Q4 2025 data reveals:

| Metric | Figure | Context |

|---|---|---|

| Price Growth (Q4 2025) | +0.6% | Continued upward momentum |

| Full Year 2025 Growth | +3.3% | Moderated from previous years |

| Resale Transaction Share | 52.7% | Majority of market activity |

| New Sale Share | 48% | Strong developer sales |

| Recent PSF Range | $2,600 - $6,500 | Varies by location and property type |

HDB Resale Market Dynamics

The HDB resale segment benefits from structural demand drivers:

- Permanent residents (PRs) entering the market

- Former private homeowners completing their 15-month wait-out period

- These buyers often bring substantial gains from private property sales, supporting HDB price momentum

Property market analyses project 3-5% price growth for 2025, with sub-3% mortgage rates providing additional affordability support.

Investor Implications

For property investors, the rate environment creates nuanced opportunities:

| Factor | Impact on Investors |

|---|---|

| Lower financing costs | Improved cash flow; higher yields |

| Increased buyer competition | Potential cap rate compression |

| Rental market dynamics | Lower rates may eventually reduce rental demand as tenants buy |

| Leverage optimization | Opportunity to restructure debt efficiently |

The Affordability Equation

Lower mortgage rates directly improve housing affordability. Consider a $1.5 million condominium purchase:

| Rate | Monthly Payment (75% loan, 25 years) | Annual Payment | Qualifying Income (TDSR 55%) |

|---|---|---|---|

| 3.6% | $5,697 | $68,364 | $124,298 |

| 2.98% | $5,280 | $63,360 | $115,200 |

| Savings | $417/month | $5,004/year | $9,098 less required income |

The $417 monthly reduction and $9,000 lower income requirement expand the pool of qualified buyers, potentially supporting property values.

Expert Perspectives: What Industry Insiders Are Saying

Mortgage Broker Insights

Industry professionals at firms like Mortgage Master and 93Property offer nuanced guidance:

"Current fixed rates offer superior value compared to floating rates. The spread has narrowed to 20-50 basis points, making fixed rates attractive for most borrowers. Our advice: capitalize on this window."

On floating rate interest: "We're seeing growing interest in floating-rate loans as SORA declines, but a substantial segment of homeowners continues to favor fixed rates for the financial certainty they provide—likely shaped by recent periods of rate volatility."

Bank Strategist Views

UOB and OCBC strategists anticipate:

- Short-term Singapore dollar rates stabilizing in the 1.45%-1.6% range

- Following potential initial dips, rates expected to find a floor

- Gradual normalization rather than dramatic cuts

The SIBOR Transition Urgency

For borrowers still on SIBOR-pegged loans, the sub-3% rate environment coincides with a critical transition:

- SIBOR is being discontinued as a benchmark

- Existing SIBOR loans will transition to alternative rates

- Proactive refinancing allows borrowers to choose their new benchmark rather than accepting a default conversion

The narrowing spread between fixed and floating rates enhances the appeal of refinancing to a fixed-rate package before any forced transition.

Action Steps: Your Refinancing Checklist

Immediate Actions (This Week)

-

Review your current loan statement

- Confirm your current interest rate

- Identify lock-in expiry date

- Note any clawback clauses from previous refinancing

-

Calculate your break-even

- Use the framework in this article

- Factor in all costs including penalties

-

Check your eligibility

- Review TDSR position

- Gather income documentation

- Check credit report for issues

Short-Term Actions (Next 30 Days)

-

Obtain competing quotes

- DBS: Request 2.98% package details

- OCBC: Request matching quote

- UOB: Request alternative structure

- Consider mortgage brokers for wider comparison

-

Evaluate fixed vs. floating

- Assess your risk tolerance

- Model scenarios based on SORA forecasts

- Consider hybrid structures

-

Understand all terms

- Lock-in period length

- Penalty structures

- Partial prepayment allowances

- Notice period requirements

Decision Point (Within 60 Days)

- Make your move

- Submit application to chosen lender

- Lock in rate (most banks offer 30-60 day rate locks)

- Coordinate with existing lender for smooth transition

Food for Thought: Questions to Guide Your Decision

-

Certainty vs. Optimization: If you could lock in 2.98% today or potentially get 2.75% in 6 months (with a 30% chance of rates rising to 3.3% instead), which would you choose? How does your answer reflect your true risk tolerance?

-

The Lock-In Paradox: Banks offer penalty waivers for property sales during lock-in periods, but does this inadvertently encourage you to treat your home as a tradable asset rather than a long-term residence? How might this shape your property decisions over the next 3-5 years?

-

Wealth Preservation vs. Cash Flow: A 2.98% rate saves you $137,000 in total interest over 24 years but only $478 monthly. Would you rather have the psychological comfort of lower monthly payments or the mathematical satisfaction of minimized lifetime interest? What does your preference reveal about your financial priorities?

-

The SORA Bet: If you believe SORA will fall to 1.5% by 2026, a floating rate could save you money. But if you're wrong and SORA stays at 2.5%+, you'll pay more than the fixed rate. Given that professional economists disagree on the trajectory, what information do you have that gives you confidence in your prediction?

-

Systemic Implications: If sub-3% rates stimulate a property market rebound in 2025-2026, could this trigger policy responses (cooling measures, supply increases) that ultimately work against property values? How should you factor potential government intervention into your timing decisions?

Conclusion: Seizing the Sub-3% Window

The return of mortgage rates below 3%—led by DBS's 2.98% fixed-rate offering—represents a genuine inflection point for Singaporean property owners. After years of elevated borrowing costs, this shift creates tangible opportunities to reduce monthly payments, minimize lifetime interest, and optimize your property financing strategy.

The key is informed, timely action. For those out of lock-in, the math overwhelmingly favors refinancing. For those still within lock-in periods, careful break-even calculations will reveal whether paying penalties makes sense. First-time buyers gain improved affordability, while investors can optimize leverage across their portfolios.

The competitive response from OCBC and UOB will likely maintain pressure on rates, but the direction of travel matters as much as the absolute level. With SORA projected to decline through 2025, the window for securing attractive fixed rates may be narrower than it appears—once rates bottom, the best opportunities will have passed.

As you navigate these decisions, remember that property financing is not a one-time event but an ongoing optimization process. The choices you make today should align with your 5-year, 10-year, and 25-year financial objectives, not just your immediate monthly cash flow.