If you're a first-time HDB buyer in 2026, the Singapore government is essentially offering you the deal of a lifetime: a CPF housing grant stack worth up to S$230,000 — enough to wipe out roughly a quarter of the cost of a median 4-room resale flat before you even sign the Option to Purchase. That's the headline number making the rounds in property chats, WhatsApp groups, and BTO ballot post-mortems. But like most things in Singapore property, the fine print decides who actually walks away with the full payout and who gets a fraction of it.

This is the playbook. We'll break down each grant in the stack, explain the eligibility flow, run four real-world buyer profiles through the numbers, and show you exactly how the CPF housing grant 2026 framework compares between resale and BTO. By the end, you'll know which lever to pull to maximise your own first-timer grant entitlement — and which decisions could quietly cost you tens of thousands.

Background: Why 2026 Is the Most Generous Grant Year on Record

The current grant framework is the product of two big policy shifts. First, on 20 August 2024, the government raised the Enhanced CPF Housing Grant (EHG) ceiling from S$80,000 to S$120,000 for families — a 50% uplift in a single move. Second, in October 2024, BTO classifications were restructured into Standard, Plus, and Prime categories, with the June 2026 launch being the first where roughly half the new supply falls into the subsidy-clawback Plus/Prime tiers.

The combined effect: resale flats — which can access the entire grant stack — became substantially more competitive against BTOs, especially for buyers who want to live near family or need immediate occupancy.

Here's how the maximum stack has evolved over the years:

Maximum First-Timer Grant Stack Over Time (S$)

A few quick definitions before we go deeper:

- First-timer: You have never received a subsidised housing benefit before (no previous BTO, no previous Family Grant, etc.).

- HFE Letter: The HDB Flat Eligibility letter — the single official document that tells you exactly which grants you qualify for. You apply via the HDB Flat Portal before committing to any flat.

- MOP: Minimum Occupation Period (5 years for Standard BTOs; 10 years for Plus/Prime).

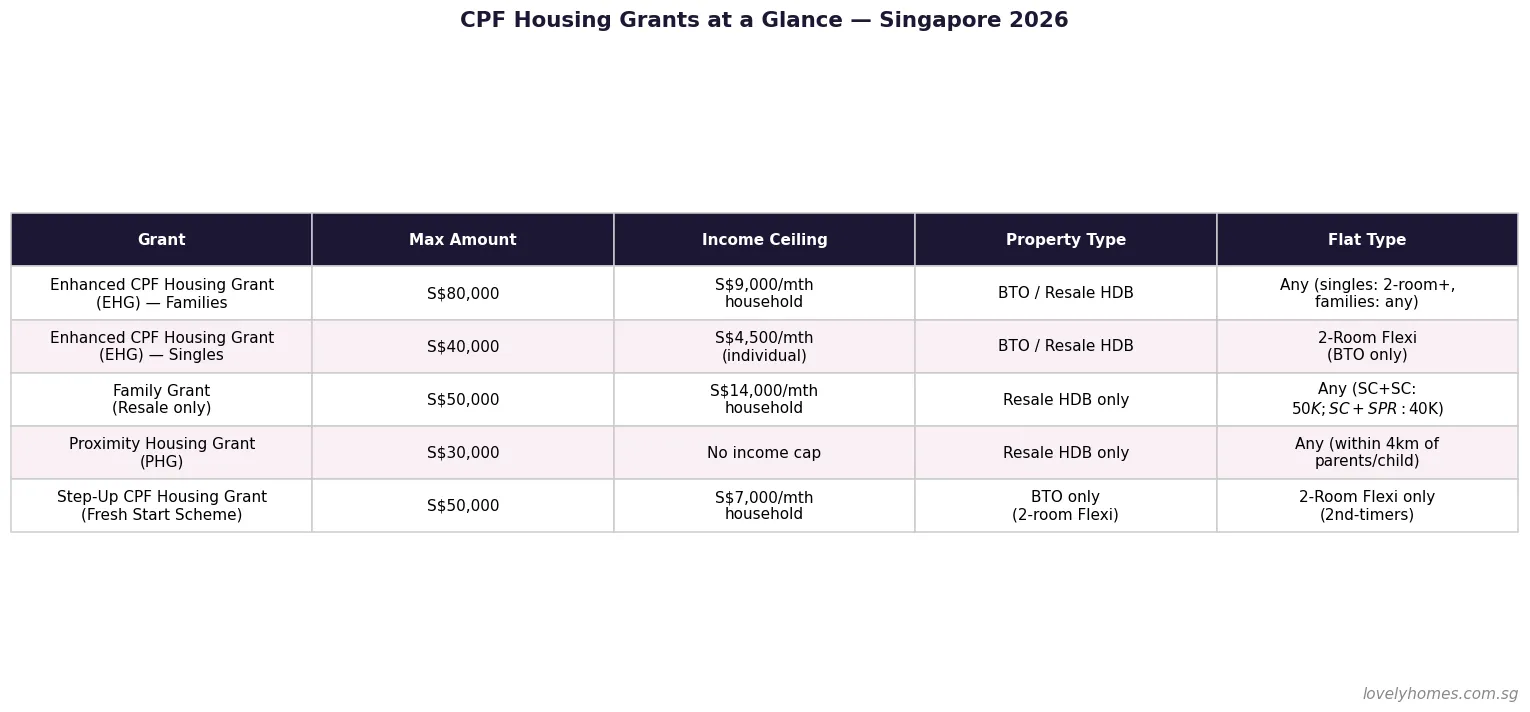

The Four Grants That Make Up the S$230K Stack

The maximum stack of S$230,000 is built from three components for a first-timer family buying a small resale flat near their parents:

| Grant | Maximum (Families) | Maximum (Singles) | BTO eligible? | Resale eligible? |

|---|---|---|---|---|

| Enhanced CPF Housing Grant (EHG) | S$120,000 | S$60,000 | ✅ | ✅ |

| CPF Housing Grant (Family/Singles) | S$80,000 (family) / S$40,000 (singles) | S$40,000 | ❌ | ✅ |

| Proximity Housing Grant (PHG) | S$30,000 | S$15,000 | ❌ | ✅ |

| MAXIMUM STACK | S$230,000 | S$115,000 | S$120K cap | Full stack |

The crucial takeaway: BTO buyers only get the EHG. The other two grants — Family/Singles and PHG — are resale-only. This single fact reshapes the entire BTO-vs-resale debate for 2026.

Enhanced CPF Housing Grant (EHG)

EHG is the largest single component of the stack — and the most income-sensitive. The lower your household income, the higher your payout. Here's the full table (effective 20 August 2024) for families:

| Avg Monthly Household Income | EHG Amount |

|---|---|

| ≤ S$1,500 | S$120,000 |

| S$1,501–2,000 | S$110,000 |

| S$2,001–2,500 | S$105,000 |

| S$2,501–3,000 | S$95,000 |

| S$3,001–3,500 | S$90,000 |

| S$3,501–4,000 | S$80,000 |

| S$4,001–4,500 | S$70,000 |

| S$4,501–5,000 | S$65,000 |

| S$5,001–5,500 | S$55,000 |

| S$5,501–6,000 | S$50,000 |

| S$6,001–6,500 | S$40,000 |

| S$6,501–7,000 | S$30,000 |

| S$7,001–7,500 | S$25,000 |

| S$7,501–8,000 | S$20,000 |

| S$8,001–8,500 | S$10,000 |

| S$8,501–9,000 | S$5,000 |

| > S$9,000 | Not eligible |

EHG (Families) Drops Sharply With Income

Singles get exactly half the family amount in each bracket, with a tighter income ceiling of S$4,500 (or S$9,000 if buying jointly with another single, or buying a resale flat with parents). Maximum singles EHG: S$60,000.

Two important EHG fine-print rules:

- 12-month employment rule: You must have worked continuously for 12 months immediately before the HFE application. Career gaps or fresh graduates take note.

- Lease coverage: Buyers aged 55+ only get the full EHG if the remaining lease covers the youngest owner to age 95. Otherwise, the grant is pro-rated.

CPF Housing Grant (Family Grant) — Resale Only

This is the "classic" Family Grant — and crucially, it's only available on the open-market resale, not BTO.

| Flat Type | SC + SC | SC + SPR |

|---|---|---|

| 2- to 4-room | S$80,000 | S$70,000 |

| 5-room or larger | S$50,000 | S$40,000 |

Income ceiling: S$14,000 (S$21,000 for extended families).

Notice the penalty on 5-room flats: you lose S$30,000 simply by upsizing. This is a deliberate nudge toward smaller flats — and the reason the S$230K maximum stack only works on a 2-, 3-, or 4-room.

Singles Grant — Resale Only

| Flat Type | Amount |

|---|---|

| 2- to 4-room | S$40,000 |

| 5-room (joint singles only) | S$25,000 |

Income ceiling: S$7,000. Like the Family Grant, this is resale-only.

Proximity Housing Grant (PHG) — Resale Only

The PHG is the only grant in the stack with no income ceiling, which makes it accessible even to higher-earning households who get nothing from EHG.

| Living arrangement | Families | Singles |

|---|---|---|

| Living with parents/children | S$30,000 | S$15,000 |

| Living within 4 km of parents/children | S$20,000 | S$10,000 |

The catch: you must commit to the proximity arrangement for 5 years — the same length as the MOP. PHG is more lifestyle commitment than tax break.

The Eligibility Flow: Who Qualifies for What

Eligibility is the gating mechanism that decides whether your stack is S$5K or S$230K. Here's the decision flow:

Three layers of checks really matter:

- Citizenship structure: SC + SC couples get the full amounts. SC + SPR couples lose S$10K on the Family Grant.

- Income ceiling cascade: Each grant has its own ceiling — S$9K for EHG, S$14K for Family Grant, and none for PHG. A household earning S$10,000/month can still get S$80K Family Grant + S$30K PHG = S$110K, even with zero EHG.

- Mode of purchase: BTO unlocks only EHG. Resale unlocks the entire stack.

All of this is calculated for you when you apply for the HFE Letter via the HDB Flat Portal — and we strongly recommend doing this before you even start viewing flats. The HFE returns a personalised grant figure so you know your actual cash position, not the theoretical one.

Resale vs BTO: The Grant Maths That Reshapes the Decision

Here's the comparison that should anchor every first-timer's buying decision in 2026:

| Buyer Profile | Maximum BTO Grants | Maximum Resale Grants | Resale Advantage |

|---|---|---|---|

| First-timer family (SC+SC) | S$120,000 | S$230,000 | +S$110,000 |

| First-timer family (SC+SPR) | S$120,000 | S$220,000 | +S$100,000 |

| First-timer single | S$60,000 | S$115,000 | +S$55,000 |

Maximum Grant Stack: BTO vs Resale (S$)

A S$110,000 swing in favour of resale is huge. But — and this is the standard caveat — BTO flats are priced below market, so a portion of that gap is closed by the lower headline price. With the new Plus and Prime classifications, however, that BTO discount comes attached to a 10-year MOP and a 6–9% subsidy clawback on first resale, plus a S$14,000 resale-buyer income ceiling. For Plus/Prime buyers, the lifetime grant value is meaningfully worse than the Standard BTO of yesteryear.

The decision tree for a first-timer family in 2026 looks something like this:

Four Buyer Profiles: Worked Examples of the Stack

Theory is one thing; numbers are another. Here are four realistic buyer profiles run through the 2026 grant framework.

Profile A — Young Working Couple (Lower-Middle Income)

- Combined income: S$5,500/month (two early-career professionals).

- Purchase: 4-room resale flat in Sengkang, within 4 km of parents.

| Grant | Amount |

|---|---|

| EHG (S$5,001–5,500 bracket) | S$55,000 |

| Family Grant (4-room, SC+SC) | S$80,000 |

| PHG (within 4 km) | S$20,000 |

| Total Stack | S$155,000 |

This is one of the most common real-world scenarios — and it still nets S$155K of grants.

Profile B — Middle-Income Couple at the EHG Edge

- Combined income: S$8,800/month.

- Purchase: 5-room resale flat in Tampines, co-living with parents.

| Grant | Amount |

|---|---|

| EHG (S$8,501–9,000 bracket) | S$5,000 |

| Family Grant (5-room, SC+SC) | S$50,000 |

| PHG (living with parents) | S$30,000 |

| Total Stack | S$85,000 |

The lesson here: once you push above S$8,000/month combined, EHG falls off a cliff. The Family Grant and PHG carry most of the stack value. Buyers near the income ceiling should think carefully about timing — a year-end bonus or promotion can wipe out tens of thousands in EHG eligibility.

Profile C — The Theoretical Maximum Stacker

- Combined income: S$1,400/month.

- Purchase: 4-room resale flat, co-living with parents.

| Grant | Amount |

|---|---|

| EHG (≤ S$1,500 bracket) | S$120,000 |

| Family Grant (4-room, SC+SC) | S$80,000 |

| PHG (living with parents) | S$30,000 |

| Total Stack | S$230,000 |

This is the celebrated S$230K maximum — and it's real. The realism caveat: a household at S$1,400/month rarely has the savings buffer or HDB loan capacity to clear a median 4-room resale price of S$650K–S$1M in mature estates. The maximum stack is more often achieved in non-mature estates where flats are still in the S$450K–S$600K range.

Profile D — Single Buyer Near Parents

- Income: S$4,200/month.

- Purchase: 3-room resale flat within 4 km of parents (35+ years old).

| Grant | Amount |

|---|---|

| EHG (Singles, ~S$4,001–4,500 bracket) | ~S$25,000 |

| Singles Grant (3-room) | S$40,000 |

| PHG (Singles, within 4 km) | S$10,000 |

| Total Stack | ~S$75,000 |

Singles have improved substantially since 2024, but still get roughly half the family equivalents. The theoretical singles maximum — S$115,000 — requires income ≤ S$1,500/month and living with parents.

Market Context: Why Grants Matter More Right Now

The grant stack lands in a 2026 resale market that's showing the first signs of softening after a multi-year run-up:

- HDB Resale Price Index (Q1 2026): 203.4, down 0.1% q-o-q — the first quarterly decline since Q2 2019.

- Resale volume: 6,285 transactions in Q1 2026 — down ~4.5% YoY but up ~17.6% q-o-q.

- Million-dollar flats: A record 412 transactions in Q1 2026 alone; 1,594 for full-year 2025, up 54% YoY.

Million-Dollar HDB Resale Transactions

Median 4-room resale prices in mature estates (Q1 2026):

| District | 4-Room Median | 5-Room Median |

|---|---|---|

| Queenstown | S$1.038M | — |

| Toa Payoh | S$1.000M | S$1.10M |

| Bukit Merah | S$938K | S$1.085M |

| Ang Mo Kio | — | S$1.09M |

Run the maths on Profile A's S$155K grant stack against a S$650K non-mature 4-room: the grants offset roughly 24% of the price. For Profile C's S$230K theoretical maximum on the same flat: 35%. That brings the effective net price into territory genuinely comparable to a Standard BTO in a non-mature estate.

Recent Policy Changes You Need to Know

The grant landscape has moved quickly. Here's the recent timeline:

| Date | Change |

|---|---|

| 20 Aug 2024 | EHG raised: families S$80K → S$120K; singles S$40K → S$60K. HDB loan LTV cut from 80% → 75%. |

| Oct 2024 | New BTO classification: Standard / Plus / Prime replaces the mature/non-mature framework. |

| 2025 | Fresh Start Grant raised to S$75,000; DIA scheme relaxed; Singles can now buy 3-room and select 4-room BTO in any estate. |

| 8 May 2026 | EC MOP extended to 10 years; 90% first-timer quota for 2 years; Deferred Payment Scheme removed. |

| June 2026 | First BTO launch where Plus/Prime makes up ~50% of new supply. Plus/Prime resale buyers capped at S$14,000 income. |

The trajectory is clear: more help for first-timers, more friction for everyone else. The Aug 2024 LTV cut, the EC May 2026 reset, and the EHG bump are all part of a coherent policy stance against speculation and in favour of owner-occupiers.

Five Strategies to Maximise Your Stack

Putting it all together, here are the levers a first-timer can actually pull in 2026:

- Apply for the HFE Letter first — before viewing flats. It eliminates guesswork on your specific grant entitlement.

- Buy resale to unlock the full stack — especially if you're near the EHG income cliff. The S$110K resale advantage doesn't exist for BTO buyers.

- Stay under the EHG income ceiling at the time of HFE application — even by a few hundred dollars. Bonuses paid before application count; bonuses paid after don't.

- Live near (or with) your parents — PHG has no income ceiling and is the easiest grant to capture if your lifestyle already aligns.

- Don't oversize the flat — moving from a 4-room to 5-room costs you S$30,000 in Family Grant. Buy what you need, not what you can stretch to.

Food for Thought

- If you're a young couple earning S$8,000/month combined today and expecting promotions, is it worth applying for an HFE letter now to lock in the higher EHG bracket — even before you've found a flat?

- The S$230K stack rewards smaller flats. Does the policy framework risk creating a generation of first-timer households squeezed into 3- and 4-room units when families are growing again?

- With Plus/Prime BTOs imposing 10-year MOPs and clawbacks, will the resale market structurally outperform BTO for first-timers over the next decade — or will Standard BTO supply quietly catch up?

- The Proximity Housing Grant explicitly subsidises multi-generational living. Should the framework also subsidise proximity to work or childcare, given Singapore's evolving family structures?

- If you're a single buyer earning above S$4,500, the entire EHG is closed to you. Is it time for the singles framework to mirror the family income tiers more closely?

Conclusion

The S$230,000 first-timer grant stack is real — but accessing the full amount requires a very specific combination of low household income, a 2- to 4-room resale flat, and proximity to family. For most working couples in 2026, a realistic stack of S$100K–S$160K is the more honest figure to plan around. Even at that lower number, grants offset a meaningful share of the entry-level resale price, and resale's grant advantage over BTO is now larger than it has been in years.

The right strategy comes down to your specific income, family structure, and timeline — and the difference between an optimal stack and a suboptimal one can easily be S$50,000 or more.